Irs Tax Code Flooring

4 43 1 Retail Industry Internal Revenue Service

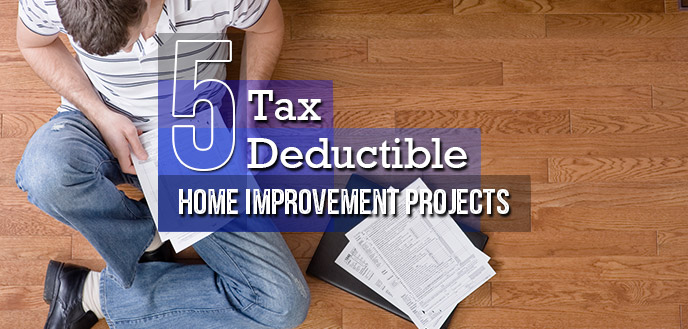

5 Tax Deductible Home Improvements For 2018 Budget Dumpster

Irs Home Office Tax Deduction Rules Calculator Home Trends Home Home Office

Covid 19 Relief For Entities With Income Not Effectively Connected To U S Trade Or Business

What To Do When You Receive An Irs Audit Letter Atlanta Tax Lawyers

Internal Revenue Bulletin 2020 15 Internal Revenue Service

Then select the activity that best identifies the principal source of your sales or receipts for example real estate agent.

Irs tax code flooring.

Find The Right Tax Attorney Get Tax Relief In Illinois Other Areas Business Tax Settlement Corp

Are Home Improvements Tax Deductible It Depends On Their Purpose Business Insider

Tax Debt Collection Compromise Levy Liens Lawyers Silver Law Plc

Tax Deductions For Individuals A Summary Everycrsreport Com

What Is Code Section 6056 For Health Care Reform Turbotax Tax Tips Videos

Irs Releases 2021 Amounts For Health Savings Accounts Gelman Llp Cpas Advisors

What Is The Irs Form 1099 Misc Turbotax Tax Tips Videos

Cedar Park Round Rock Irs Tax Attorney

Can I Still Deduct The Costs Of Entertaining Customers Under The New Tax Law World Floor Covering Association

Pin On Just Build Wealth

You Won T Believe How Complex Our Tax System Is Here S How To Make Sense Of It Us Tax The Motley Fool Believe

Abandonment Of Commercial Property Using The Internal Revenue Code 263 A Tangible Property Regulations Capital Review Group

Irs Plr 202012003 Cold Storage Warehouse Fti Consulting

Kbkg Tax Insight Qualified Improvement Property Qip Technical Correction In Cares Act Kbkg

Loans Between Related Entities Tax Law For The Closely Held Business

Kbkg Tax Insight Impact Of Bonus Depreciation For Companies With Floor Plan Financing Kbkg

Tax Help In 2020 Investing Money Tax Checklist Tax Help

What The Irs Says About Business Appraisals Appraisers

Federal Tax Attorneys York Pa

Tax Deductions For Working From Home

Irs Moves Chna Due Dates To December 31 2020

6 Red Flags That Can Trigger An Irs Tax Audit Angie S List

:max_bytes(150000):strip_icc()/business-executives-discussing-in-office-meeting-997745894-9e19b97892a34b509370afeff80663f9.jpg)

Describing A Passive Foreign Investment Company Pfic

Tax Breaks For Capital Improvements On Your Home Houselogic

Self Employed Individuals Tax Center Federal Income Tax Tax Guide Internal Revenue Service

Tax Code Changes Leave Americans Asking What Happened To My Refund Work Family Tax Tax Accountant

Estate Tax In Bellflower Tax Services Estate Tax Bookkeeping Services

Why Is The Irs Punishing Triple Net Landlords Tax Lawyer Filing Taxes Irs Penalties

Lifetime Learning Credit Internal Revenue Service Federal Taxes Employer Identification Number

Gross Rent Floor Allocation And Placed In Service Default Novogradac

2020 2q Irs Interest Rates In 2020 Tax Lawyer Business Tax Tax Attorney

Tax Law Tax Forms Child Tax Credit Tax Help Tax Rebate Check State Tax Forms Homebuyer Tax Credit Tax Tips

28 W2 Form 2016 In 2020 Filing Taxes W2 Forms Online Taxes

Sbw Associates Pc Tax Briefs

How Estimated Taxes Work Safe Harbor Rule And Due Dates 2020 With Images Safe Harbor Estimated Tax Payments Internal Revenue Code

Mortgage Interest Deduction Or Standard Deduction Houselogic

Fillable Online Flooring Sample Submittal Form Moldingsonlinecom Fax Email Print Pdffiller

How To Depreciate Leasehold Improvements Small Business Chron Com

How Is Flooring Depreciated In A Rental Home Guides Sf Gate

New Property For Sale Inbox Me For Any Questions 2185 Marble Avenue Spring Hill Fl 34609 Awesome Opportunity On A Great Property New Property Real Estate

Https Idahoemployeeperks Com Portals 0 Pdfs Nampafloors Pdf

Obtain A Tax Id Ein Number For Your Hair Salon Business Ein Number Application Business Help Center

Ronald Mcdonald Family Rooms Ronald Mcdonald House Charities Dayton

Federal Income Tax Guide For 2020 For 2019 Tax Prep

Source : pinterest.com